Payment receipts in government are more than proof of purchase; they are formal records that support audits, resolve disputes, and confirm that financial obligations have been met. The Canadian government processes millions of transactions each year across departments, agencies, and benefit programs, and each one generates some form of payment receipt. The type of receipt generated depends on the payment method, the system involved, and the purpose of the transaction. Understanding the different types helps departments, suppliers, and payees know what to expect and what records to retain.

What Are Payment Receipts in Government

Payment receipts in government are official records confirming that a financial transaction has taken place. They document the amount, date, parties involved, and transaction reference for every payment. In the Canadian context, these records are required by financial management policies, internal audit frameworks, and tax compliance rules.

What a Receipt Records

A government payment receipt captures specific data that serves multiple downstream purposes. At a minimum, it records the transaction amount, the payer or payee identifier, the date, and a reference number. In electronic systems, it may also include the payment method, the clearing network used, and the status at the time of generation. That data becomes the source record for reconciliation, dispute resolution, and financial reporting throughout the fiscal year.

Receipts vs Confirmations: A Practical Distinction

Payment receipts and payment confirmations are related but serve different functions. A confirmation indicates that a payment has been initiated and is in process. A payment receipt, in the strict sense, indicates that the transaction has been recorded as complete, often with evidence of settlement. In practice, many government systems use the terms interchangeably, but the distinction matters in audit and compliance contexts where completeness of the record is assessed against both initiation and settlement data.

Why Government Receipts Follow Specific Requirements

Government payment receipts are not generated by choice; they are required by policy. Treasury Board of Canada Secretariat financial management policies require departments to maintain records of all financial transactions. The CRA requires businesses to keep receipts and supporting documents for at least six years, per its records retention rules. For government departments, these retention obligations apply to both incoming and outgoing payment records, covering everything from supplier invoices to benefit disbursements.

Why Payment Receipts Matter for Government Agencies

Payment receipts matter because they are the evidence base for everything that happens after a transaction. Without them, departments cannot reconcile their accounts, respond to payee inquiries, or demonstrate to auditors that controls were followed. Every claim of compliance in government financial management ultimately rests on the quality and completeness of the payment receipt record.

The scale of what is at stake became visible in recent years. The Office of the Auditor General of Canada’s 2024 Commentary on Financial Audits reported that post-payment verifications identified almost $6 billion in overpayments or payments to ineligible COVID-19 benefit recipients in 2023–24. Accurate payment receipt records were central to identifying and recovering those funds. Gaps in receipt documentation were among the control weaknesses cited by auditors in that same report.

- Audit trail creation: Every payment receipt creates a time-stamped record that auditors use to verify that transactions were authorized, processed, and recorded correctly.

- Dispute resolution: When a payee reports a missing or incorrect payment, the receipt record is the starting point for tracing what happened.

- Reconciliation support: Finance teams match payment receipts against bank statements and payment registers at the end of each settlement cycle.

- Compliance evidence: Regulators, internal auditors, and oversight bodies all use payment receipt records to test if financial controls are working.

- Year-end reporting: Confirmed payment receipts are the source data for departmental financial statements and consolidated government accounts.

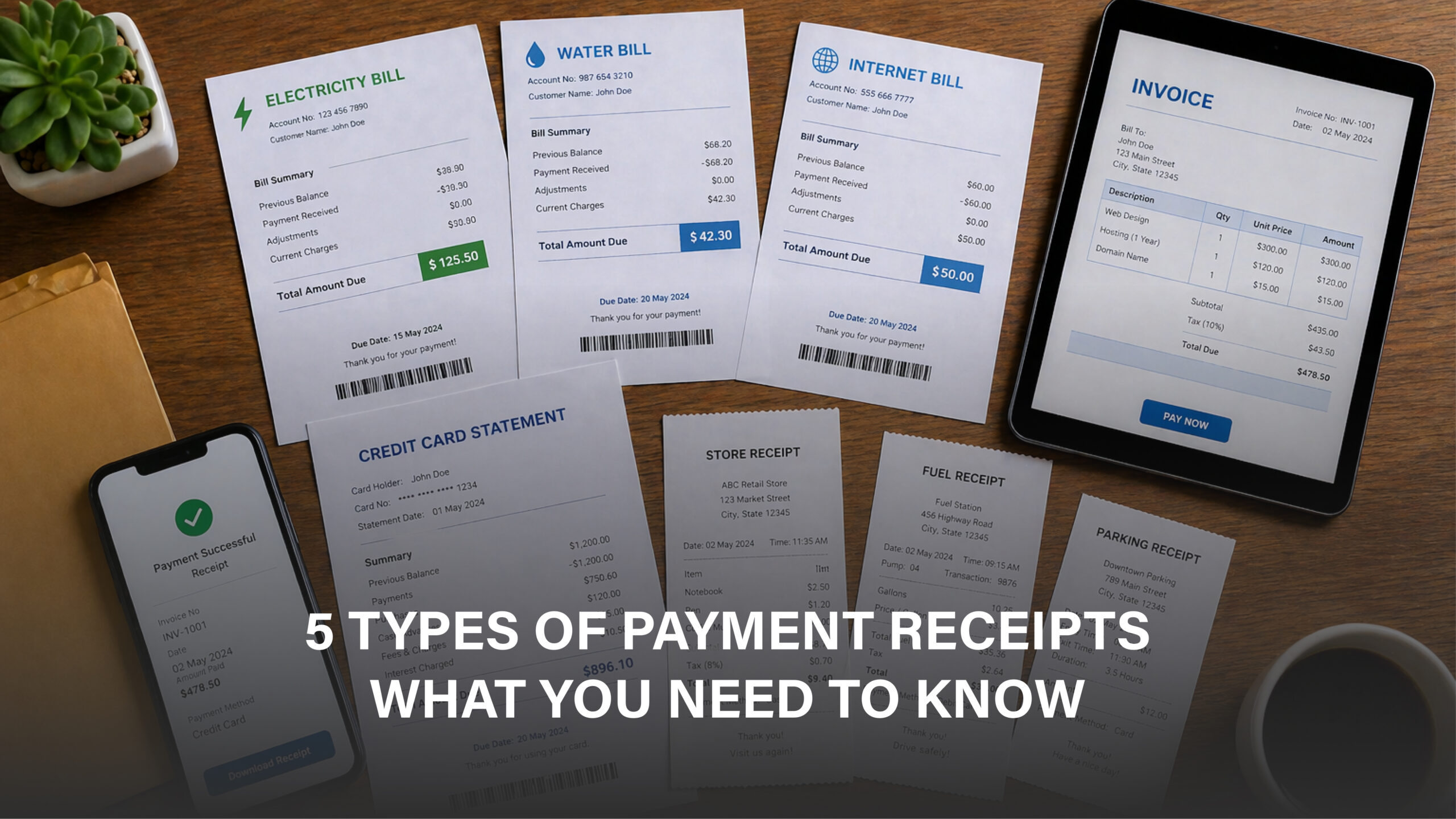

The 5 Types of Payment Receipts Used in Government

Government agencies use five distinct types of payment receipts depending on the system, payment method, and transaction purpose. Each type serves a different role in the overall record-keeping framework. Understanding what each one captures and where it is used helps departments and payees know which records to request and retain.

1. Digital Payment Receipts

Digital payment receipts are system-generated records produced automatically when a transaction is processed in an electronic payment system. They are instant, traceable, and stored in the payment system’s database alongside the transaction data.

In Canadian government contexts, digital receipts appear in CRA’s My Account, departmental supplier portals, and payroll systems when a payment is confirmed. They carry a transaction reference number, a timestamp, and often a payment status that updates immediately as the transaction progresses through settlement.

Digital receipts are the most commonly encountered type in modern government payment systems.

According to Payments Canada’s 2025 Canadian Payment Methods and Trends Report, digital payments represented 86% of total payment volume in Canada in 2024. That dominance is reflected in how government payment systems generate and store receipts. The vast majority of government payment receipts are now digital, which means they are searchable, retrievable, and auditable at scale.

2. Bank or Transaction Receipts

Bank receipts are issued by financial institutions as confirmation that a specific transaction was processed through their systems. In government payment contexts, these appear as payment-advice files, account debit confirmations, or direct deposit notices.

They provide third-party evidence of settlement that is independent of the government’s internal record. When a question arises about if a payment has been settled after confirmation, the bank receipt is the definitive record that resolves it.

Bank receipts carry the account numbers, routing information, transaction date, and settlement amount for each payment. They are used in reconciliation to match the government’s internal payment confirmation record against the bank’s settlement record.

Any discrepancy between the two is flagged for investigation. For payees who receive payments by direct deposit, the bank receipt is visible as a transaction description in their account statement, often labelled with the department name or a payment reference code.

3. Acknowledgement Receipts

Acknowledgement receipts confirm that a submission has been received but do not confirm that settlement has occurred. In government systems, these are common at the point of application or request submission.

When a taxpayer submits a return through CRA’s online portal, they receive an acknowledgement that the submission was accepted. When a supplier submits an invoice through a government procurement portal, an acknowledgement confirms that the invoice has entered the system.

Neither of these constitutes a payment receipt in the full sense; both indicate a step in the process, not its completion.

The distinction matters in dispute resolution. If a payee believes they submitted an invoice but the department has no record of it, an acknowledgement receipt proves the submission occurred and when.

This shifts the investigation from “did they submit?” to “what happened after submission?” Departments that generate and retain acknowledgement receipts at every intake point reduce the number of disputes that cannot be traced and resolved quickly.

4. System-Generated Payment Confirmations

System confirmations are backend records generated automatically by government ERP and payment management systems when transaction status changes. They are used primarily for internal tracking rather than payee-facing communication.

When a payment moves from “approved” to “confirmed” in an accounts payable module, the system creates a confirmation record against the transaction reference number. This record is what finance teams search for when reconciling payment runs and what auditors examine when testing if controls were applied at the right stage.

System confirmations differ from digital receipts in their audience and format. A digital receipt is typically formatted for the payee and delivered through a portal or email. A system confirmation is a database entry visible to department finance staff and accessible through reporting tools.

Both serve essential functions, but they serve different stakeholders. Departments that treat system confirmations as internal-only records and fail to make corresponding receipt data available to payees create unnecessary inquiry volume when payees cannot find their own transaction records.

5. Manual or Paper Receipts

Paper receipts remain in use in specific government transaction contexts, particularly for legacy payment processes, in-person transactions, and high-value cheque payments.

A department that issues a cheque to a vendor may generate a paper disbursement voucher as the receipt record. An agency processing a cash payment at a service counter generates a manual receipt at the point of transaction.

These records are then scanned or entered into the department’s financial system to create a digital copy alongside the paper original.

Paper receipts carry inherent risks: they can be lost, damaged, or misfiled before digitization occurs. Despite this, their use persists in part because cheque payments remain significant in total value.

According to Payments Canada’s analysis of Canada’s future in real-time payments, cheques still accounted for $2.7 trillion in payment value in 2024 despite a 10% year-over-year volume decline.

For transactions of that scale, paper receipt processes are still encountered in certain government and B2B contexts. Departments are encouraged to digitize paper receipts promptly after creation to preserve the audit trail.

How Payment Receipts Are Generated in Government Systems

Payment receipts in government are generated at multiple points in the payment lifecycle, not just at the moment funds are settled. Each generation event creates a record tied to a specific transaction stage.

At the Point of Payment Initiation

When a payment is initiated through a government ERP or payment management system, the system generates an initial record tied to the transaction. This may take the form of an order number, a requisition confirmation, or an early-stage system receipt.

It is not a final payment receipt, but it anchors all subsequent records to the same reference identifier. This anchor record is what allows finance teams to reconstruct the full payment history of any transaction from initiation through settlement.

At Confirmation and Settlement

The most significant receipt generation event occurs when a payment is confirmed and settled. At confirmation, the internal payment system creates a record updating transaction status. At settlement, the banking system generates a corresponding bank receipt or payment-advice file.

These two records together form the complete payment receipt for the transaction. Reconciliation is the process of matching these two records against each other after each settlement cycle.

Through Self-Service Portals

Many government agencies now give payees direct access to their payment receipts through online portals. CRA’s My Account, myBenefits CRA, and departmental supplier portals all allow payees to retrieve receipt records for past transactions. This reduces inquiry volume to department finance teams and ensures payees have access to the records they need for their own accounting and compliance purposes. Portals that generate and display payment receipts automatically also reduce the risk of receipt records being lost or unavailable when they are needed for an audit.

Key Information Included in Government Payment Receipts

A government payment receipt must contain enough information to serve its three core functions: proving a transaction occurred, enabling tracing and reconciliation, and supporting audit review. The specific fields vary by payment type, but a complete payment receipt includes a standard set of data elements.

- Transaction reference number: A unique identifier that links the receipt to the internal system record, the bank record, and any related documents like invoices or purchase orders.

- Payment date and time: The timestamp of when the receipt was generated, which establishes the fiscal period for reporting and the baseline for late payment interest calculations.

- Payer and payee details: The department or agency name and the payee identifier, which may be a vendor number, a social insurance number, or a business number, depending on the transaction type.

- Payment amount: The exact amount transacted, including any applicable taxes or deductions that affect the gross or net figure.

- Payment method: The channel through which payment was made: direct deposit, wire transfer, cheque, or electronic data interchange.

- Status at time of receipt: The transaction status recorded at the moment the receipt was generated: confirmed, settled, returned, or reversed.

- Issuing system reference: An identifier for the system or department that generated the receipt, which allows the record to be traced back to its source during audit or investigation.

Payment Receipts vs Payment Confirmations

Payment receipts and payment confirmations are often used interchangeably in government contexts, but they refer to different points in the transaction lifecycle. Knowing the distinction helps departments maintain accurate records and helps payees understand what each document actually proves.

What a Confirmation Establishes

A payment confirmation establishes that a payment has been initiated and processed through the government’s internal system. It records that the transaction is in motion. Confirmation does not prove that funds have reached the payee’s account. In many government systems, the confirmation is generated before the payment file is even sent to the bank, which means a confirmed status can exist alongside a payment that has not yet settled.

What a Receipt Establishes

A payment receipt, used precisely, establishes that the transaction is complete. It combines the confirmation record with the bank settlement record to prove that funds moved from the government account to the payee. Not all government systems generate a single document that covers both stages. In practice, the complete payment receipt is often assembled from two records: the internal confirmation and the bank payment advice file. Finance teams and auditors treat both together as the full receipt for a settled payment.

Why the Distinction Matters in Practice

The distinction matters most in three situations: dispute resolution, year-end reporting, and audit review. In a dispute, a payee who received a confirmation but no funds needs the bank receipt to determine what happened at settlement. For year-end reporting, only payments with both confirmation and settlement records are classified as completed expenses. In an audit review, an auditor who sees confirmation records without corresponding bank receipts will flag the gap as an incomplete audit trail, which generates a finding regardless if any funds were lost.

Common Challenges in Managing Payment Receipts

Managing payment receipts in government systems at scale introduces predictable challenges. Most arise from the combination of multiple systems, high transaction volumes, and legacy processes that were not built to work together. Recognizing these challenges is the first step toward managing them effectively.

- Inconsistent formats: Different departments and systems generate payment receipts in different formats, which complicates cross-department reconciliation and makes unified reporting difficult.

- Missing bank receipts: Internal system confirmations are often easier to retrieve than the corresponding bank payment-advice files, leaving the bank-side record of settlement harder to locate when needed.

- Paper receipt digitization gaps: Paper receipts that are not promptly digitized can be lost before they enter the permanent record, creating gaps in the audit trail for specific transactions.

- Portal access limitations: Some payees do not have access to self-service portals that display their receipt records, which means they depend on department staff to retrieve documents on request.

- Retention period confusion: Different types of payment receipts have different retention requirements, and departments do not always apply the correct standard to each document category.

- Duplicate records: System errors or manual reprocessing can generate multiple receipt records for the same transaction, creating confusion during reconciliation without careful duplicate detection.

Compliance and Audit Requirements for Payment Receipts

Government payment receipts are subject to financial management policies, audit standards, and records retention requirements that are more prescriptive than those in the private sector. Compliance in this area is not optional; it is a condition of operating within the federal financial management framework.

Treasury Board Policy Requirements

The Treasury Board of Canada Secretariat’s Policy on Financial Management requires departments to maintain complete and accurate records of all financial transactions. This includes payment receipts at every stage of the transaction lifecycle, from initiation through settlement and any subsequent adjustments. Departments are expected to have systems in place that allow any transaction to be traced from its original authorization through its final disposition. A payment without a complete receipt trail is treated as a control failure, regardless if the funds were properly spent.

CRA Records Retention Rules

The Canada Revenue Agency requires that payment records be retained for a minimum of six years from the end of the tax year to which they relate. This applies to both the government’s own financial records and to businesses and individuals interacting with government payment systems. Electronic records are accepted provided they are kept in a readable format and available on request. Physical receipts that have been digitized meet CRA requirements as long as the digital copy is a complete and accurate representation of the original.

Auditor General Standards

The Office of the Auditor General of Canada applies financial audit standards that require payment receipts to support every material transaction in a department’s financial statements. Auditors test if receipt records exist, or they are complete, and even if they are consistent with bank settlement data. Departments that cannot produce receipt records for sampled transactions receive audit findings that may affect their overall audit opinion. Consistent receipt documentation practices are among the clearest ways a department can demonstrate financial management maturity to its auditors.

Best Practices for Managing Payment Receipts in Government

Effective payment receipt management requires more than generating records when a transaction occurs. It requires a consistent approach to storage, retrieval, retention, and reconciliation that holds across all payment types and all departments involved.

- Generate receipts at every stage: Create a receipt record at initiation, confirmation, and settlement so the full transaction lifecycle is documented without gaps.

- Retain bank receipts alongside internal ones: Internal system records and bank payment-advice files together form the complete receipt; keeping only one creates a partial audit trail.

- Digitize paper receipts promptly: Paper receipts should be scanned and entered into the financial system the same day they are generated to prevent loss before digitization.

- Apply consistent reference numbers: Use the same transaction reference number across all receipt types for a given payment so records from different systems can be matched quickly.

- Give payees receipt access: Self-service portal access for payees reduces inquiry volume and ensures receipt records are available to both parties without manual retrieval requests.

- Apply correct retention periods: Different receipt types have different minimum retention periods; classify each type at creation and apply the appropriate standard.

- Reconcile receipts regularly: Match internal confirmation receipts against bank settlement receipts at least weekly to catch discrepancies before they affect financial reporting.

How Digital Systems Improve Payment Receipt Tracking

Digital systems change how payment receipts are generated, stored, and retrieved in ways that directly improve compliance and audit readiness. The shift from paper-based to electronic receipt management is already well underway in Canadian government payment systems, and the benefits compound as adoption increases.

Automatic Generation and Storage

Digital payment systems generate receipts automatically at each transaction stage without requiring manual action. There is no delay between the transaction event and the creation of the receipt record. Storage is immediate and searchable. Finance staff can retrieve any receipt by transaction reference, date, or payee without navigating physical files. This automation reduces the risk of missing receipts and makes reconciliation significantly faster than in paper-based environments.

Immediate Reconciliation

Digital systems that integrate internal payment records with bank settlement data immediately to allow reconciliation to happen continuously rather than at the end of a reporting period. Discrepancies between the internal confirmation receipt and the bank settlement receipt are flagged automatically rather than discovered during a manual review cycle. This shortens the time between a payment error occurring and its detection, which reduces the risk that errors compound or affect financial statements before they are corrected.

Audit Readiness by Default

When digital systems generate and retain complete receipt records automatically, departments are audit-ready at all times rather than only during audit preparation periods. The Office of the Auditor General provided unmodified audit opinions for 68 of 70 federal government organizations it audited in 2024–25, per its 2024–25 Commentary on Financial Audits. Departments with consistent digital receipt practices are among those better positioned to maintain that standard. Gaps in receipt records remain one of the most common sources of audit findings in the organizations that do not receive clean opinions.

Payment Receipts Are the Foundation of Government Financial Accountability

Every payment processed through a government system leaves a receipt trail, and the quality of that trail determines how well a department can account for its financial activity to auditors, oversight bodies, and the public. The five types of payment receipts used in government each serve a specific purpose, and gaps in any one category create downstream problems that are difficult and time-consuming to resolve. Access2Pay supports government departments in generating, managing, and retrieving payment receipts with the accuracy and consistency that compliance and audit requirements demand.